One woman weathers a career change and upside-down car loan to pay off $133,000 in debt

One-third of adults age 30 or younger have student loan debt, with the median burden hovering at $17,000. In Debt Diaries, we introduce you to those who took on their debt and came away with a better understanding of themselves. Their testimonials offer hope -- and tools -- to show that you, too, can overcome debt.

Amanda Williams is the founder and owner of Debt Free in Sunny CA, where she helps guide others to debt-free living by sharing tips, and fostering an in-person and online community. She and her husband, Josh, celebrated paying off more than $133,000 in debt in less than four years on July 5, 2018.

How Amanda’s student loan debt began

I took out private student loans to go to school for massage therapy. After graduating, I worked on several cruise ships massaging clients for eight to 10 hours a day. The repetitive strain led to carpal tunnel and I was not able to return to massage therapy. At 22, I went back to school for computer science and used student loans to pay my tuition. While in school, I worked full time to pay my rent and bills.

At the time, I was working a minimum wage job, which doesn't get you much in California. There was no way I was going to be able to save up to pay for school, so I took out loans because that's what you do when you're going to school -- or so I thought.

I would have done more research on my school and the actual cost of it instead of saying, "Oh, that's fine, I'll pay it back later," not realizing how much money and interest I'm actually going to be paying. If I had done my research, I could have saved a lot of money by going to a different school at the beginning.

Living with debt

Right after I graduated with my bachelor's degree, I was in the six-month grace period, where you don't have to pay on your student loans. I was having fun the first few months, and then I got down to business and was like, "OK, these payments are coming. In a few months, I’ll have this $433 car payment and this expensive student loan balance coming." I wasn't making enough to pay both of them.

There was no big fat raise when I finished school and received my degree. That's when panic set in.

It felt like there was a dark cloud over my head. I looked at this giant number and thought how am I going to pay that off on what I make now? It's going to take me forever. It was not a good mental state to be in—kind of depressing.

Picking a plan, paying up and getting ahead

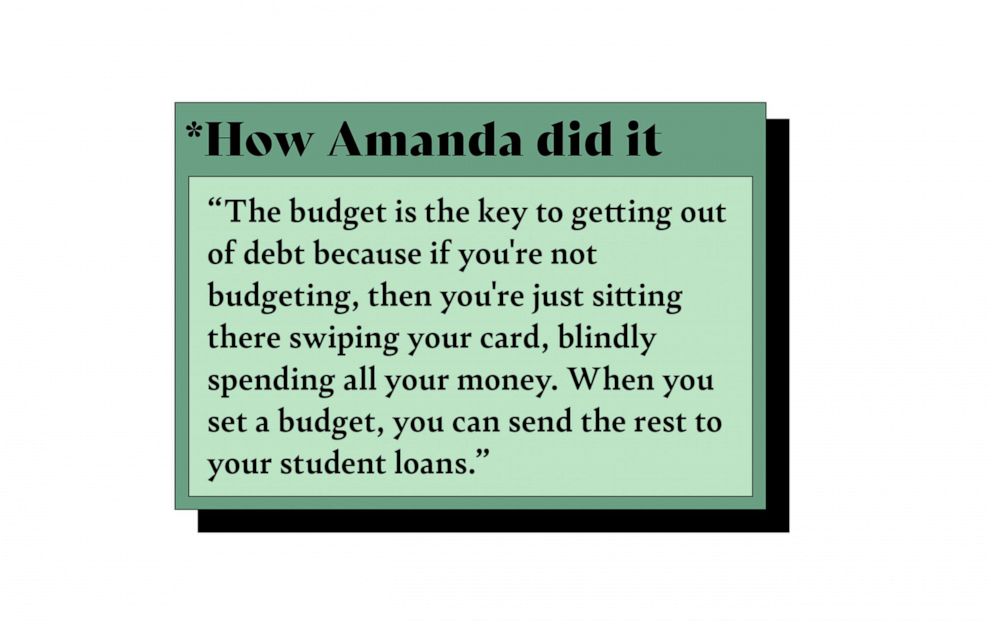

My first idea was to follow Dave Ramsey's "Total Money Makeover" because I liked how he lays out the baby steps. What really helped was getting on a budget and actually saying, "OK, I’m going to spend this much on groceries, this much on gas," etc. It was hard at first because in the past, I just used a card, bought what I needed and then paid it off. But that's paying for the past. Switching to "this is what I'm going to spend," and then figuring out how to adjust it and make it work made a huge difference. Once I had the budget dialed in, anything extra went towards the smallest balance loan. That was the game plan going in.

I was able to get an internship while in school that paid $14 an hour. From that experience, I jumped over to a large company that offers education reimbursement. The rest of my bachelor's degree and all of my master’s degree was covered by my company.

I reached out to other people online who are doing the same thing -- budgeting and paying off their debt. Having people online that are going through the same thing really helped keep me motivated.

I started using my personal Instagram profile to search hashtags like "debt free" or "Dave Ramsey" to find other people. There weren't a whole lot of people posting about getting out of debt, so that's when I created my own profile and started the hashtag. Then it just blew up. There are tons of people now sharing their journey of getting out of debt on Instagram.

I sold the Prius that I could not afford, and it was a tough pill to swallow because I was upside down on the loan. It was one bad mistake after another. I took out the full value of a previous car to "pay off" my private student loans. When I traded the car in for a Prius, I rolled the negative equity into the car loan. I was upside down by $7,000. It took me eight months to make the decision on if I should sell or keep the car.

You have to make big sacrifices to get out of debt.

It was a noticeable transition that really hit me when I thought about what I wanted. Did I want a nice car and to be in debt for longer or did I want to drive around in a not-so-nice car and be debt-free much faster? It was a mindset shift for what I wanted for my life.

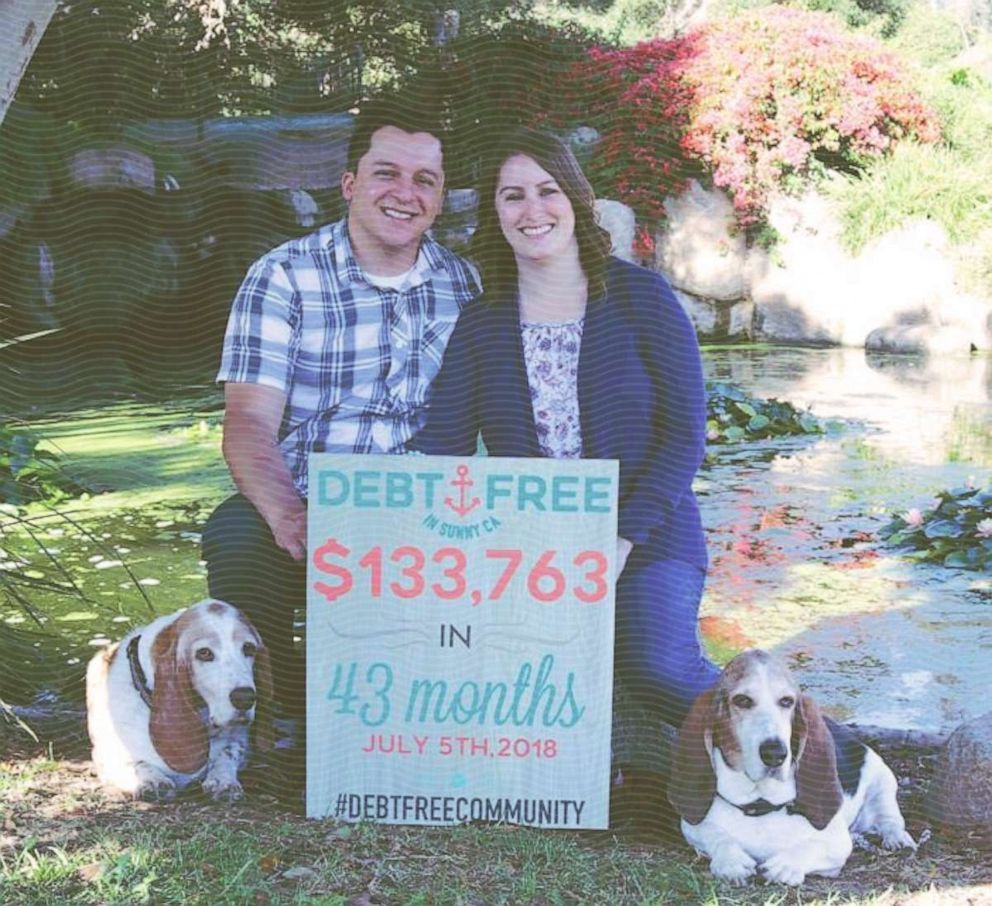

The Big Payoff

The years of hard work to get to this point -- you're just kind of numb, like, "Oh my gosh, we did it!" It took us three years and four months to pay off all of our debt -- together, we had over $133,000 worth of debt.

To celebrate, we took the day off work and went to brunch. We met up with friends for dinner to celebrate.

Now we're completing our emergency fund and saving up as much as we can for our first baby. Our emergency fund will be six months of our expenses, which works out to be $15,000 to $20,000.

We just paid for a new-to-me car in cash and have plans to start investing in real estate.

Her message to you

I suggest getting an internship in your field as soon as possible and trying to find a company that provides education reimbursement.

The budget is the key to getting out of debt because if you're not budgeting, then you're just sitting there swiping your card, blindly spending all your money. When you set a budget, you have the freedom to decide what you want to do with your money.

Also, you need to have an emergency fund. That way you're not reliant on credit cards and, when something comes up, it's not a catastrophe. You're relaxed, you've got the money and you can take care of it.

My debt free journey has taught me delayed gratification. If there’s something I want to buy, I save up and pay cash for it.

I want to emphasize that I started with a low income. Through my education and getting an internship early, I was able to get my foot in the door and work my way up to the salary I make now. A lot of people focus on the ending salary and think that they can't do it. I want to give hope to people that if they put in the hard work, they will get there, too.

If, along the way, your finances have been affected by COVID-19, reach out to your providers and ask what assistance they can offer. Waived late fees and deferred payment plans are common options. Also, cut any unnecessary expenses to help stretch your budget.

You can follow Amanda’s continuing journey and get more tips on living a debt-free life by following her on Instagram at Debt Free in Sunny CA.